With less than four weeks of frantic trading left to run, SUV sales to the end of November – as shown in VFACTS figures released this week – have climbed 15.9 per cent over the same 11-month period in 2014, compared to 1.3 per cent for light commercial vehicles (LCVs), 2.3 per cent for heavy commercials (HCVs) and, tellingly, minus 3.1 per cent for passenger cars.

With another negative return for passenger cars last month (-3.1%), and further double-digit growth for SUVs (+16.2%), the distance between the two broad sectors has continued to close to the point where less than 100,000 units separate them (471,511 versus 373,032) – not a huge margin by any stretch when you consider that this time last year the gap was 165,000.

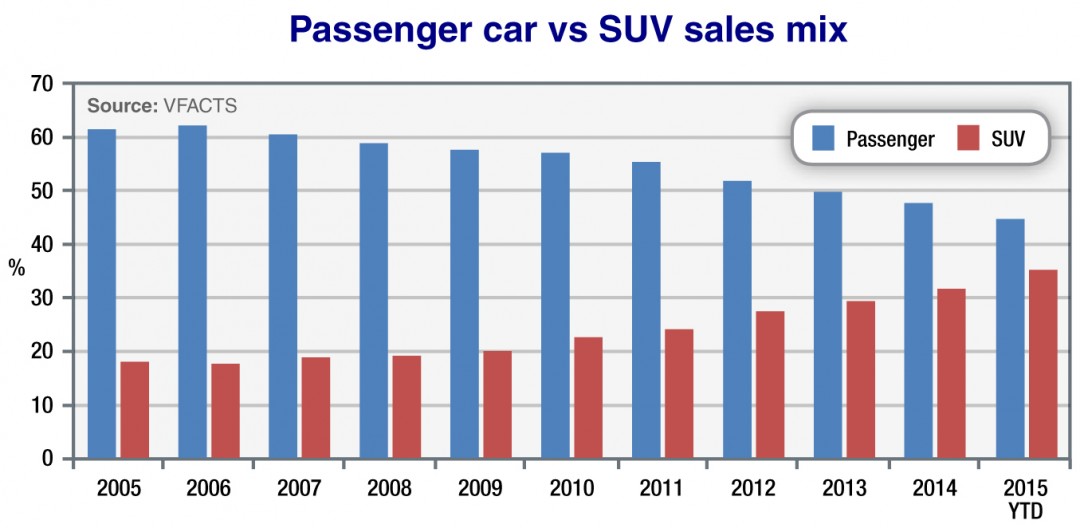

As it stands now, passenger cars account for 45 per cent of the total market, compared to SUVs on 35 per cent, LCVs on 17 and HCVs on three. Last year, the passenger/SUV sales mix was 48:32, and the year before that it was 50:29. In 2010 the mix was 57:23, in 2005 it was 62:18, and in 2000 it was 70:13.

Stretching that far back, SUV was not even part of official industry lexicon – it was ATW (all-terrain wagon) or simply 4WD, which underscores the subsequent market shift to a wide variety of more passenger-car-like models with an “on- road” orientation and no absolute requirement for four-wheel drive, let alone a low-range transfer case or the like.

The sales mix shows incremental shifts that have slowly gained momentum and are now clearly an insurmountable tide.

Within the broad passenger car sector, the biggest-selling segment – small cars – has fallen 7.0 per cent this year, while micro-cars are down 31.3 per cent, large cars are 9.6 per cent in arrears and upper-large cars are 20.5 per cent worse off than they were a year ago. Sportscars have also taken a 4.2 per cent hit.

Xanadu: Fiat’s new 500X crossover adds more weight to the burgeoning SUV segment and provides another reason for Australian buyers to consider a small high-riding wagon over a traditional passenger car.

That leaves only three segments in positive territory – light cars (+4.6%), medium cars (+8.7%), and the niche people-mover class (+16.5 per cent).

By comparison, sales have grown in each of the four SUV segments this year, with the burgeoning small SUVs leading the charge with a 28.1 per cent volume increase, followed by medium SUVs (+15.5%), large SUVs (+9.1%) and upper-large SUVs (+4.0%).

This is not a licence to print money for all companies offering SUVs, with Chery, Dodge, Fiat, Ford, Jeep, Mini, Peugeot and Volvo among those down across their SUV stable this year, but there are 22 other brands (or 76 per cent of those still active in the market) experiencing growth.

In the passenger car segment there is an even split between those experiencing growth and those who are down among the 40-plus brands in the market this year, but note that seven of the top-10 volume-selling brands in Australia are in a negative position – Mazda, Hyundai, Holden, Ford, Mitsubishi, Nissan and Honda – along with high-profile marques such as Alfa Romeo, Chrysler, Fiat, Lexus and Porsche.

This, in turn, puts an increasingly heavy emphasis on SUVs – and LCVs where models are available – within each brand’s overall sales performance, as shown by Mazda which has already passed its 2012 full-year record with a month still to run (104,316 sales YTD, +13.4%), but has struggled all year with its top-selling Mazda3 small car (-10.9%).

Fiat’s launch of the 500X small SUV this week typifies how car-makers are pulling out all stops to get into the fastest-growing market segment in Australia and a host of other countries.

Participation is no guarantee of success, but the mere fact of its arrival – and the millions of dollars pumped into advertising and other publicity measures – will generate more interest in the genre and, if not leading directly to sales for Fiat, will benefit its competitors as prospective buyers compare it with other brands.

SUV specialist Jeep, for instance, sold only 50 examples of its new Renegade in November – its first full month on sale and a surprisingly low result for such a new and high-profile vehicle (built off the same platform as 500X) – whereas Mazda sold around 1400 examples of the CX-3, Mitsubishi shifted more than 1100 examples of its ageing but clearly evergreen ASX while Honda (HR-V), Nissan (Qashqai) and Holden (Trax) each added more than 800 to their running total.

Mazda CX-3

The mid-size SUV segment, deemed ‘small’ before the even smaller crossover segment took off, and the large SUV class (aka ‘medium’ not so long back), are attracting fewer all-new category entrants – notwithstanding some significant new additions from premium brands and in the harder-core end of the market – but are, for now at least, the two biggest-selling SUV segments.

While popular in their own right, these more established segments are also clearly benefiting from the influx of buyers brought into showrooms by the new breed of small SUVs, and who find a larger vehicle more suitable for their requirements.

As Nissan and Mazda, for example, shifted plenty of small SUVs last month, their mid-size X-Trail and CX-5 were, respectively, the number one and two biggest-selling SUVs in the entire market, each selling around 2200 units.

Medium and large SUVs are the second and third most popular segments in the entire industry, deferring only to small passenger cars, while small SUVs look certain to next year knock off light cars as the fourth most popular segment overall – if they don’t do it in the next four weeks.

And that is without Toyota in the picture, yet. Once the dominating market leader has a contender, and other major brands such as Hyundai (with an ix35 replacement) and Kia (with an all-new model) enter the fray, stand by for the inevitable changing of the guard as SUVs finally overtake passenger cars and complete the high-ride revolution once and for all.

By Terry Martin

Read More: Related articles

Read More: Related articles