The cost structure of most dealerships is fixed and new-car sales and servicing are the biggest contributors to the bottom line.

With EVs becoming the focus of the showroom, the service aspect almost evaporates and new cars become the dominant earner, requiring big management changes to reduce costs.

Right now, the dealership world is sitting on the precipice of a monumental change from which there is no known white knight. The solution to the problem exists, but it requires the dealers to take the initiative and kill a major sacred cow in the process.

Every day the following happens in the automotive marketplace:

- Another Electric Vehicle (EV) model enters the market

- Another Original Equipment Manufacturer (OEM) makes its brand agency

- Another brand makes its EV brand a ‘separate division’ to the Internal Combustion Engine (ICE) brands

- Another model stops being produced as an ICE vehicle

Every day the following happens to a dealer:

- Another model has no service / parts future

- Another dealership has no goodwill value

- another dealer has less new cars to sell into the future

- Another customer loses the chance to buy the car of their dreams

Much of how dealers integrate and participate in a world of mostly EV new vehicles is unknown. The only known is the sales model that dealers operate under today will be thrown out the window and a new model of profitability will need to be developed.

To better understand where this new model of profitability will fall, it is important that we understand how dealers make money today and what will change.

The Current Dealer Profitability Model

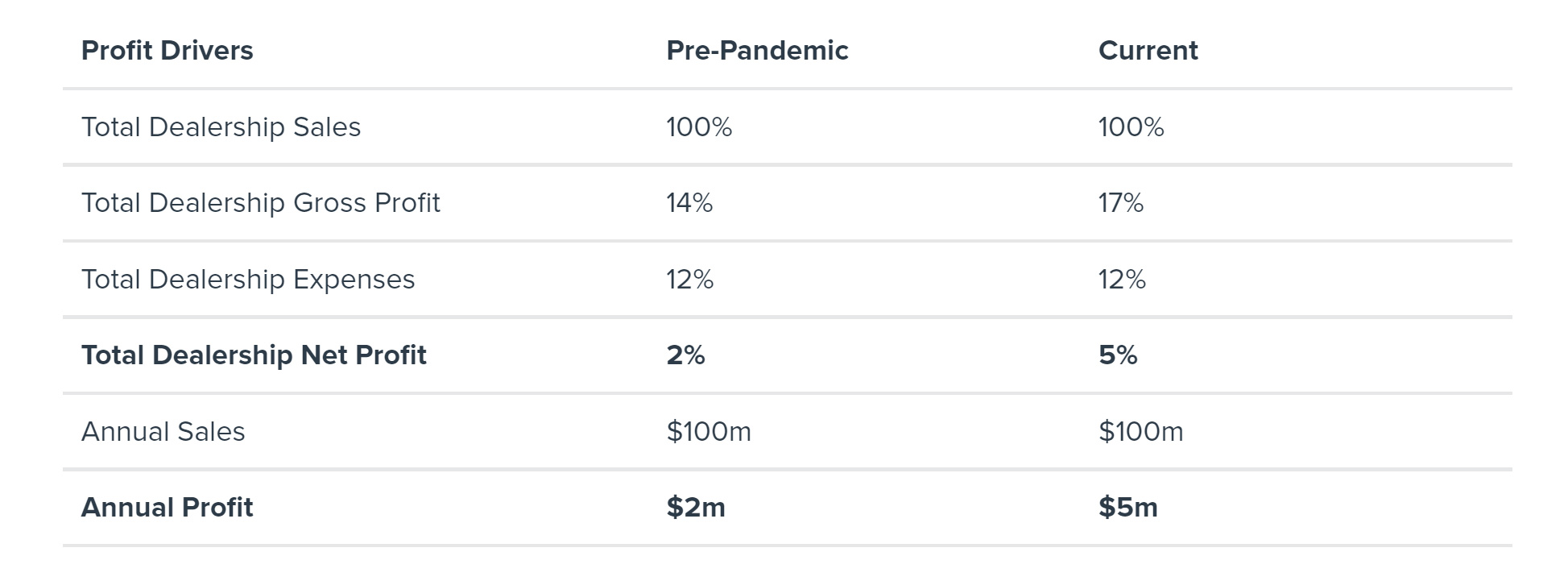

When you take it back to its core fundamentals, dealerships operate under the following basic construct:

Click image to enlarge

In dealerships, like other businesses, the major cost is people (around 70 per cent of all expenses) and the earnings and productivity of people in the industry is fairly established.

Therefore, the cost structure of most dealerships is fixed at 12 per cent of sales. To move the needle up on profitability, the key driver is gross profit and this is derived from the transactional gross profitability of each item sold by the dealership.

Given dealerships operate under a franchise model and marginality is in someway controlled by the franchisor, the sales, gross profit, and net profit mix of most dealerships looks as follows:

Click image to enlarge

Click image to enlarge

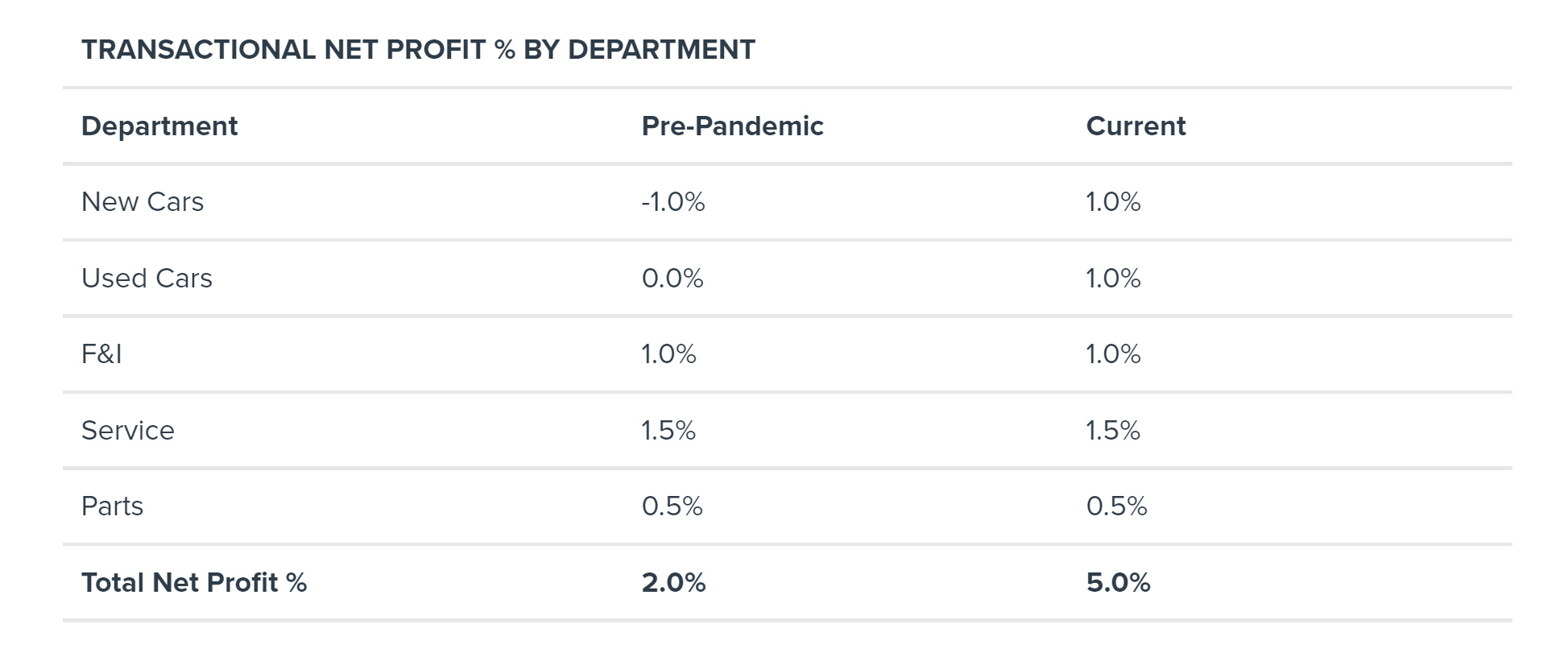

So, when you then look at the contribution to overall gross profit that each department makes to the quality of the total dealership gross profit pie, you end up with the following result:

Click image to enlarge

This is the reason that service and parts are the backbone of the business.

Prior to the pandemic creating the demand-pull front end gross profit extravaganza that is currently being experienced, fixed operations did contribute more to the overall quality of the gross profit in the dealership.

Therefore, the most profitable dealerships tended to be large service operators, these were quite often metro dealerships close to CBD’s or geographically monopolistic regional dealerships.

Often when asked to go into dealerships and turn around profitability the answer was often found in increasing service throughput, driving more used car customers into service, and implementing proper service retention strategies to drive more high-quality gross into the dealerships and push the overall gross profit percentage above 12 per cent.

This is where the adage that “you can’t sell yourself into a profit “came from in the car industry.

Making an ever-increasing number of six- and even 10 per cent new car transactions, can never increase the overall gross profit above 12 per cent without a complimentary service retention strategy.

SO, WHAT DO EV’S DO TO THIS EQUATION?

What do EVs do to this equation? We can see from the above that EV’s decimate this existing business model.

From what we know:

- EV dealer margins will be less than the pre-pandemic six per cent, and potentially under an agency model as low as two per cent of RRP.

- F&I may continue in its current form if supported by the Captive financiers, but non captive financiers and insurers are struggling with how to finance and insure these vehicles.

- Service all but disappears, with 100,000km service intervals and no Internal combustion engine to service, service revenue/gross should drop by 80 per cent.

- Parts – most parts at service relate to the ICE (filters, fluids, drive belts, fuel lines, exhaust, cooling systems). Tyres, Brakes, air conditioning, battery will still exist, but it will also decline by 80 per cent.

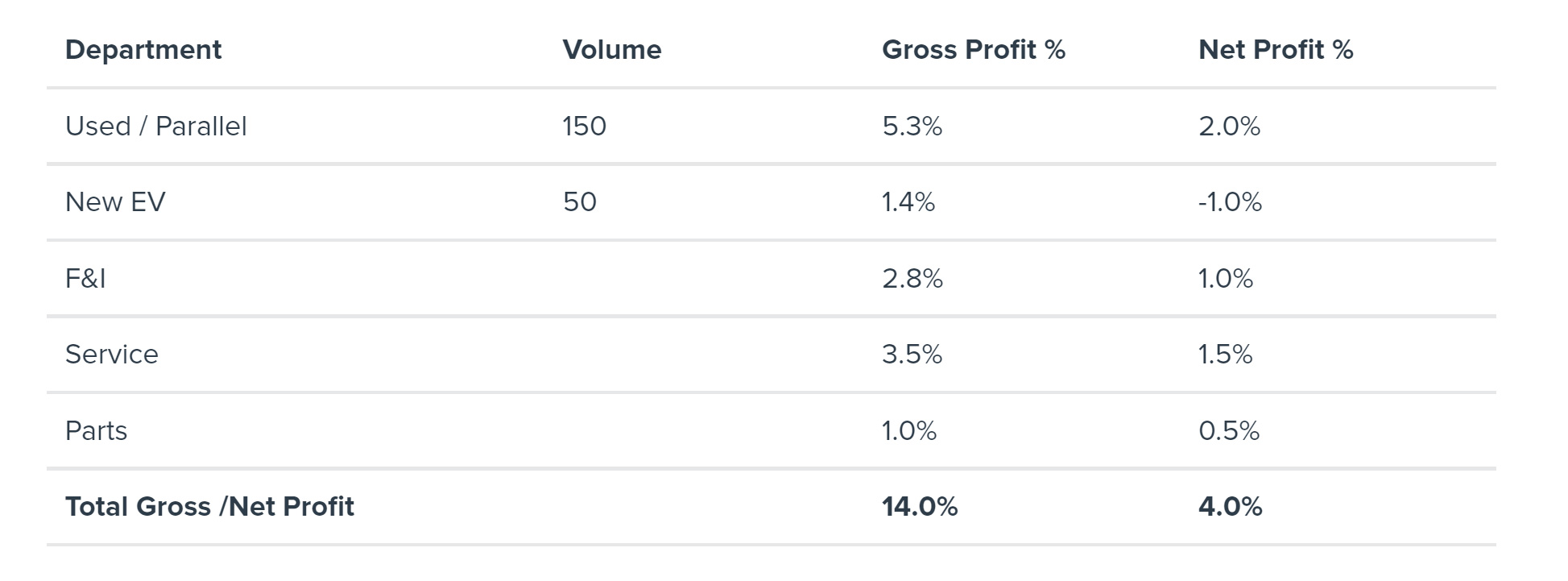

Therefore, under an EV world, assuming dealers retain the pre pandemic New Gross for EV’s, the Dealership Total Gross/ Net Profit will look as follows:

Click image to enlarge

The pull back of the dealership cost structure from 12 per cent of gross to 8.8 per cent of gross or 27 per cent is substantial.

By design this would require a dealership selling 100 new and 50 used cars a month to do the following:

- Reduce headcount from 50 to 30

- Reduce footprint by 50 per cent

- Significantly reduce management structure (higher costing people)

In the end the dealership as it is known today would fundamentally be a shop front, with little or no service presence and no support staff, all customer facing only.

The above is also made on the assumption that dealer margins remain untouched from the current arrangement and F&I arrangements continue as per the current scenario.

HOW DO DEALERS MAKE MONEY IN AN EV WORLD?

The answer is simple, remain in the Internal Combustion business by inverting your sales mix from the current dependence on new cars sales to be focussed heavily on used car sales requiring service work.

Establishing clear lines of used car supply from the local and parallel import markets, dealers need to do the following:

- Increased the used car ICE business to a minimum 3:1 used to new ratio

- Establish your own used car service business, including parts supply

- Treat all used car buying customers like you treat new car customers today

- Offer the same F&I process and aftermarket process you offer today

- Develop a strong CRM process around sales/service/sales customer retention in used cars.

- Offer limited service to the new EV customers, similarly to the service offered your used car customers today.

The EV dealer of the Future will look as follows:

Click image to enlarge

Dealers should also be able to increase their overall net profitability from the same level of turnover for the following reasons:

- Departing from the franchise based systems allows dealers to maximise their vehicle gross profitability because they will control both the purchase and sales price of their inventory , source of supply whether this be customer direct , parallel import or customer trade in will allow the dealer to pay the correct price for the trade , as opposed to the current scenario where used car prices are inflated to allow extra new car trading margin through over trading.

- By not being franchise dependent dealers will now be able to reduce their cost of customer acquisition and increase their gross by investing in independent full cycle customer journey service providers who can take more of the customer transaction online and increase the early cycle contact points.

- Dealers will be able to more cost effectively configure their real estate offerings to suit the needs of their customers. Rather than excessively large showrooms, dealers will be able to offer more open space display, more functional showroom facilities and service facilities geared towards efficient and cost-effective service requirements.

- Dealer service gross will improve while costs remain constant as vehicles outside the warranty period will be entering service in greater numbers, each offering more hours per RO. This will reduce the churn of customers through the workshop and improve customer retention as more time will be available per RO. Loan car usage will drop significantly as the numbers of jobs decline but the value per RO multiplies.

- Dealer staffing will change, DP’s, Service Managers, Parts Managers and even Service Advisors are OEM franchise constructs. Dealers will offer customers high or low touch delivery and service options based on price and technology will be used to reduce staffing costs.

- With greater customer engagement and retention as, rather than dealing with a generic franchise network, the customer now has a committed personal Dealer. This Dealer will not need to have the physicality of service linked to Sales and may opt to move service to locations more convenient to the customer cohort.

- Customer choice will flourish, this will lead to greater engagement and retention, as the focus shifts from the franchise to the customer. Product lead processes always struggle to remain profitable; Customer lead processes will always capture longer term share. Hence the reason the used car market in Australia has always been four times larger than the new car market. Dealers, through customer choice will now be playing in the big league.

CONCLUSION

For Dealers, that embrace the EV model as a means of transitioning their dealership out of the Franchise model and into the Customer Choice business will boom.

The ability to now control product choice, price, source of supply and customer engagement at a time when the ability to import vehicles is now open, is extremely exciting.

This is also coinciding with a time where the OEMs are either looking to dismantle the franchise system or limit its effectiveness with EV’s, so there will be no roadblocks to transition.

Internal Combustion Engines and Hybrids have an exceptionally long tail in Australia, there are 25 million on the roads, long distances, limited charging infrastructure and no means of out of country disposal. There is a 30-year tail which will require a minimum eight re-ownership cycles and continuous maintenance.

Creating your own franchise of choice by harnessing a market four times larger than the existing new car market is compelling.

To get on the journey, do the following:

- Start your DOC and every meeting with Used Cars.

- Make a list of the great cars you do not sell because of your franchise.

- Make your UCM the DP, he or she is the future.

- Run a list of all your used car sales customers and then a list of all your used car customers in for service and compare, then focus on reducing the gap.

- Introduce yourself to everyone buying a used car from you this month, get to know your future customer.

- Think of five ways you can make more money selling used cars (remember you control who and where you buy, the purchase price, sell price, add-ons, F&I, service plan, parts pricing) there are opportunities to make more money when you own the entire process.

Read more here:

By Stave Bragg and Wayne Pearson

Read More: Related articles

Read More: Related articles